In an ideal world, every interaction with customers would be a bed of roses. But for some businesses, a chargeback request following a customer dispute could be one of those rare, thorny moments, and a chargeback is raised. But what’s a chargeback, how do they work, and what are the best ways to protect yourself against chargeback fraud?

Chargebacks could cost your business money, so it is important to protect yourself against chargeback fraud.

What is a chargeback?

A chargeback is a reversal of a card payment after a customer sends a request to their card issuer.

Customers are entitled to submit a dispute to their card issuer and get their money back in certain circumstances, such as fraudulent charges. This will often occur following a legitimate payment dispute, but as we’ll cover later, chargeback requests could also be fraudulent. Chargebacks apply to both credit and debit card purchases.

Why do we have chargebacks?

Chargebacks are a way of giving consumers greater protection when they make a purchase. For example, it means that customers may be able to get back the money that they pay for goods or services that haven’t been delivered or are poor quality. It also gives customers the opportunity to claim money back following an unauthorised transaction.

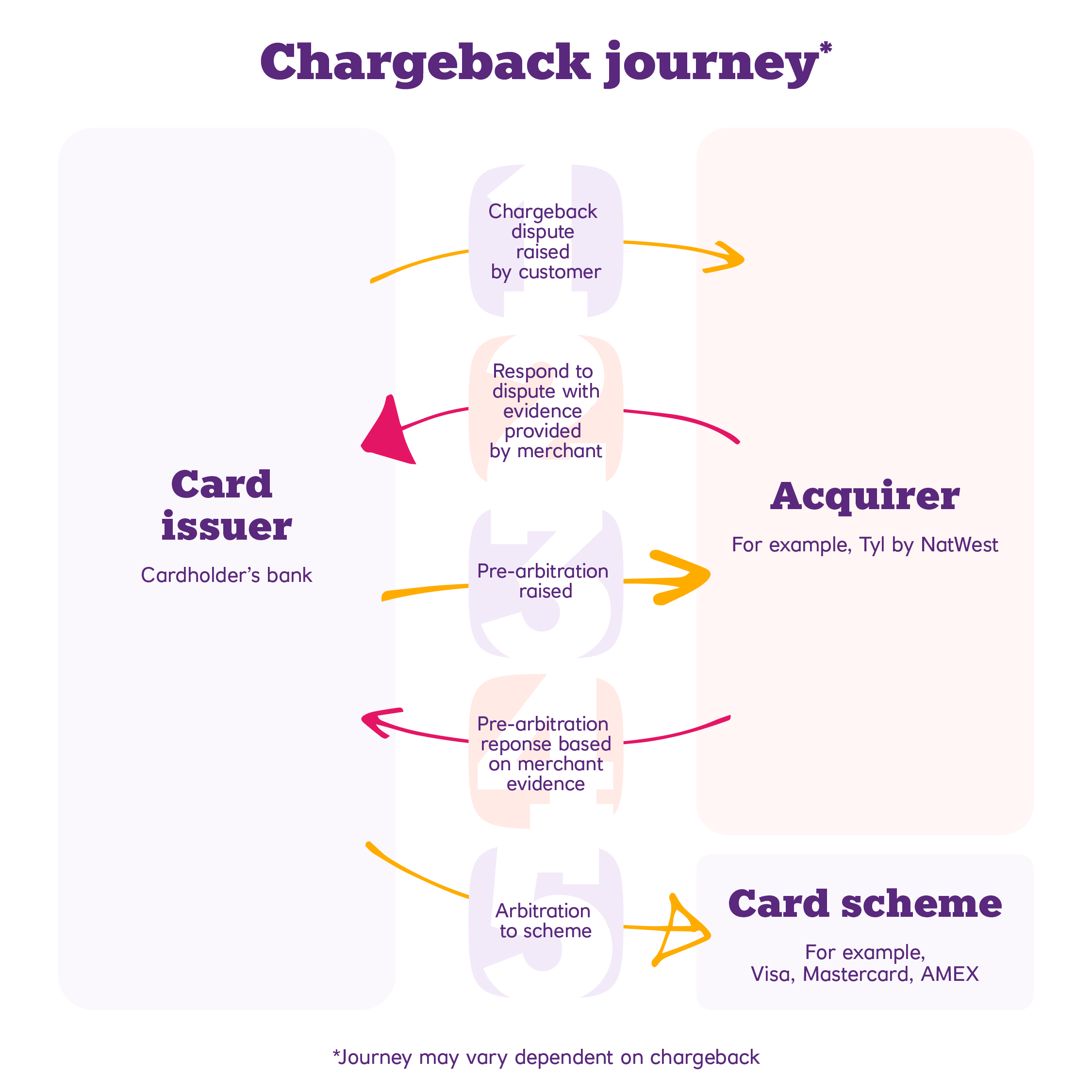

How do chargebacks work?

A customer might decide to make a chargeback claim for many reasons; for example, they might look at their bank statement and spot an item of expenditure that they don’t recognise. The customer would refer the transaction to their card issuer, such as a bank, who in turn passes the chargeback dispute to the acquirer.

The acquirer then notifies the merchant, usually by email, who will be debited for the chargeback if upheld, but will have the opportunity to provide evidence to defend the chargeback. The evidence required by the card issuer may include invoices and receipts, e-receipts or proof of delivery that show the transaction was valid and the product or service has been delivered.

If insufficient evidence is provided, then you as the merchant would have to accept the chargeback debit. If you provide evidence, the card issuer will decide whether the customer should receive their money back within an agreed timescale. You have the right to dispute the card issuers decision – a process known as arbitration. Each card scheme will have a different arbitration process along with different timescales. This could also incur further cost.

Sometimes chargeback requests are made innocently in error, or it could be a legitimate request (we’ll cover some examples later). Unfortunately, there are also some instances where someone may try to make a fraudulent claim by receiving goods, then trying to recover funds for the item(s) by claiming they hadn’t received the delivery; this is known as ‘friendly fraud’.

Responding to a chargeback request.

For Tyl customers, if a chargeback is raised against your business, we will let you know and request evidence to defend the chargeback, usually by email. Acquirers such as Tyl, are held to specific scheme rules and timings, so we’ll let you know when we need the evidence by.

It’s important to note that if you don’t respond to our request, we may not be able to defend your chargeback, leaving you liable for the chargeback amount.

Is a chargeback the same as a refund?

While it’s easy to confuse a chargeback with a refund, the two aren’t quite the same. The difference is that a refund is made by the business , while a chargeback is requested by the customer.

What are the most common reasons for chargeback requests?

A chargeback is often a last resort for a customer after they’ve unsuccessfully tried to get a refund. There are a number of instances where a customer might make a chargeback request. For example:

- They haven’t received the products or services they paid for.

- The goods they bought are defective.

- They were charged the wrong amount or the charge was duplicated.

- They were charged when they had already cancelled a subscription.

- They didn’t receive the goods they purchased because the company went out of business.

- The customer doesn’t recognise or didn’t authorise the payment.

What is chargeback fraud?

Chargeback fraud is where someone makes a purchase and then contacts their card issuer to request a chargeback without a valid reason. If you’re taking payments over the telephone, sending a payment link through a secure virtual terminal may help you reduce the risk of chargeback fraud, due to the embedded security measures.

Read our fraud prevention guide for more tips on the best ways to keep you and your customers secure. You can read more about other ways to enhance payment security, such as 3D Secure authentication checks, later in this guide.

Another type of chargeback fraud is where purchases are made on stolen cards, and the victim requests a chargeback in good faith following fraudulent activity. Card issuers often rule in favour of the cardholder in cases like these and the liability of these chargebacks often falls with you, the merchant.

How could my business prevent chargebacks?

The chances of someone filing a chargeback request may depend on the type of business you run and the way you sell products or services. See below for some tips on preventing chargeback fraud in different circumstances. If you have more questions about chargebacks, please get in touch.

Card present chargebacks

Fortunately, since the introduction of EMV technology in 1994 and subsequent chip and PIN payments ‘card present fraud’ has dramatically reduced – read more in our NFC blog. Chip technology has made it nearly impossible for criminals to use counterfeit cards and it has also reduced the risk of mass retail data hacks. However, that is not to say you should take no action to prevent fraudulent chargebacks, and many fraudsters have switched their attention to e-commerce fraud.

If you’re a face-to-face seller, you are more likely to experience duplication chargebacks – where a payment is taken more times than is necessary – and overcharge chargebacks, where a larger payment than necessary is charged, such as £500 instead of £50. To reduce the chances of these chargebacks:

- Check for errors. When keying an amount on the terminal double-check it’s correct and get the cardholder to check and agree the amount before accepting payment.

- Keep void receipts. If the payment fails, you should keep a copy of the void receipt and issue one to the cardholder. This means that in the event of a chargeback, you may be able to show that you have voided extra payments and returned them to the cardholder.

Card-not-present chargebacks

Card-not-present (CNP) payments are e-commerce or mail order/telephone order (MOTO) payments. With CNP, fraudsters may take advantage of the fact that you can’t physically check the card or meet the cardholder. One of their primary aims is to use stolen cards to obtain goods of value for resale. While you don’t want to stop any legitimate payments, it is important to manage the fraud risk of all CNP payments.

CNP transactions are less secure than card-present transactions, therefore extra care should be taken if you need to take them. Not taking CNP payments securely could not only result in a potential loss of stock, but could also leave you liable for any chargebacks raised. This would mean not only paying the cost of the chargeback, but also losing the fraudulently purchased stock.

If you take MOTO payments or sell through an e-commerce page, here are some potential ways to reduce chargeback requests:

- Authentication checks.

Use 3D Secure authentication checks if you sell through a website. If the card issuer (the bank) confirms that a card is enrolled in 3D Secure and the cardholder authentication is successful, the liability for the fraudulent transaction shifts from you, the merchant, to the card issuer. Read more about Strong Customer Authentication (SCA) . - Extra verification checks.

Consider more checks such as the Address Verification Service (AVS), which validates a customer’s billing address, and Card Verification Code (CVC) to reduce the risk of fraudulent transactions. This provides some reassurance that these details have been verified, but doesn’t guarantee that the customer is 100% genuine. This only confirms that the card details are valid, the card hasn’t been reported as lost or stolen, and that there are currently sufficient funds to cover the payment. - Tracked delivery.

If sell goods over distance, use a reputable courier or delivery service. You may be at risk of chargebacks if products arrive in poor condition or do not arrive at all, so consider using a tracked delivery service, perhaps with signature or ID request upon delivery. - Never release any goods to a third party arranged by the alleged card holder, for example a courier or taxi driver.

- If the customer decides to collect the goods, cancel the earlier transaction and take payment once more as a face-to-face chip and PIN transaction.

Other ways to reduce chargebacks

- Pre-authorised payments.

Certain sectors take payments ahead of exchanging goods or services – such as hotel bookings and car hire deposits – you may have more time to review whether a customer’s details are legitimate. You can flag any concerns with your bank before the full payment is taken. - Accurate product descriptions.

Is your product or service exactly what it says on the tin? Having clear copy that describes your items accurately could set realistic expectations and reduce the chances of a chargeback request. - Return and refund policies

Publishing a clear return and refund policy on your business website and displaying this on your premises could ensure your customers fully understand their rights and only make valid chargeback claims. - A payment gateway.

If you take payments online, having a secure payment gateway could give you and your customers some confidence that only genuine transactions will be processed. - Be identifiable.

Ensure your business name displays correctly and clearly on both customer receipts and customer bank statements, so customers are clear on where they made the payment. - Document any conversations you have with your customers as a backup, in case you need to provide evidence in future.

Your next steps:

- Review your return and refund policies and ensure they are visible.

- Ensure your trading name is correct on customer correspondence.

- Ensure detailed customer interactions and records are being kept.

- Implement fraud prevention measures and tools like AVS, CVV checks and two-factor authentication.

- Review your current process for taking payments when a card is not present.

Disclaimer

Tyl fees and eligibility criteria apply.

This has been prepared by Tyl by NatWest for informational purposes only and should not be treated as advice or a recommendation. There may be other considerations relevant to you and your business so you should undertake your own independent research.

Tyl by NatWest makes no representation, warranty, undertaking or assurance (express or implied) with respect to the adequacy, accuracy, completeness, or reasonableness of the information provided.

Tyl by NatWest accepts no liability for any direct, indirect, or consequential losses (in contract, tort or otherwise) arising from the use of the information contained herein. However, this shall not restrict, exclude, or limit any duty or liability to any person under any applicable laws or regulations of any jurisdiction which may not be lawfully disclaimed.